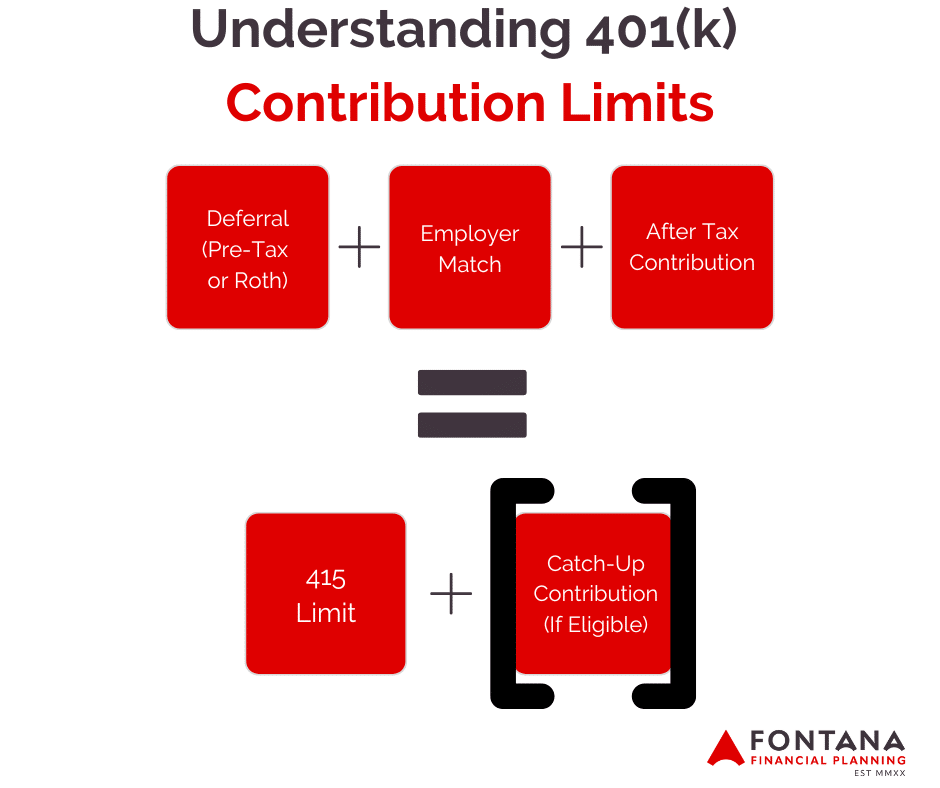

When it comes to making 401(k) contributions there are two sets of limits that an individual must be aware of – the first being the maximum deferral limit and the second being the total contribution (or 415) limit.

The maximum deferral limit represents the total amount that you as an individual can contribute to your 401(k) through either traditional or Roth contributions. For 2024, this limit is $23,000 and goes up to $30,500 for those over the age of 50 after adding in the additional $7,500 catch-up contribution those individuals are eligible to make.

The 415 limit represents the total dollars that can be contributed to a 401(k) in a given tax year. The limit for these dollars is $69,000 for the year 2024 and goes up to $76,500 for those 50 years or older. There are three components that are factored into the 415 limit:

- Traditional or Roth contributions

- Employer contributions

- After-tax contributions

To provide an example, let’s assume that you are under the age of 50 and choose to contribute the maximum allowed amount as a traditional 401(k) contribution – $23,000. Additionally, you receive an employer match on your contribution of $12,500. This means you are currently utilizing $35,500 ($23,000 + $12,500) of your total $69,000 415 limit.

The final way you can contribute towards that limit would be through after-tax contributions. Going back to our previous example, you still have $33,500 until you reached the 415 limit. Assuming your plan allowed after-tax contributions you could elect to make after-tax contributions of that entire amount in addition to the traditional contributions you were making to reach your 415 limit.

There are a few things you will want to know about after-tax contributions before you log into your 401(k) to begin making those contributions. First, not all plans offer an after-tax contribution option so you will want to confirm that your plan offers that option to get started – this should be outlined in the plan description documents.

Next, you will want to understand how after-tax contributions differ from traditional or Roth contributions. Similar to a Roth contribution, any money you contribute via the after-tax contribution source will be taxed as income in the year the contribution is made. That said, the growth on your contributions will be taxed as income when ultimately distributed in retirement.

Let’s assume that you contribute $10,000 in after-tax money to your 401(k) plan – this becomes your after-tax basis. If over time that money grows to $30,000 before being distributed you will receive $10,000 tax-free (similar to a Roth distribution) but will owe income taxes on the other $20,000 (similar to a traditional distribution). These funds are distributed ‘pro-rata’ so in our example $1 out of every $3 will be tax-free.

The after-tax contribution becomes most effective by completing a ‘Roth in-plan conversion’ immediately after making the after-tax contribution. When you complete a conversion, this takes the after-tax money and turns it into Roth money – allowing the growth to receive favorable Roth treatment upon distribution if certain conditions are met.

You will want to complete the conversion as soon as possible after contribution to optimize the tax-efficiency of the strategy. If you contribute $10,000 in after-tax funds, there are no taxes owed on the basis when it is converted. On the other hand, if the $10,000 has grown to $12,000 before the conversion is completed then you will owe income taxes on the $2,000 worth of growth.

If your plan allows it, you can also roll the after-tax source over to a Roth IRA (and an IRA for any growth that occurs prior to the rollover). This option is logistically more difficult and takes more time but if you do not like your 401(k) plan options or have another reasons to want to move these funds to an IRA it may be an option.

When you put all the pieces together, as we will now review, you are able to utilize the ‘Mega Backdoor Roth’ conversion. Using the same example we’ve used throughout this post, let’s assume you have contributed the maximum $23,000 that an individual under the age of 50 can contribute as a pre-tax contribution and you received a $12,500 match from your employer. You can contribute $33,500 as an after-tax contribution for the year and if you immediately convert or roll over the funds that $33,500 will receive Roth treatment in the future. All-in, you will have contributed a total of $69,000 into your 401(k) for the year. If you were over the age of 50 you could add an additional $7,500 of traditional or Roth money as a catch-up contribution for a total of $76,500.

Disclosure: This case study is for illustrative purposes only. Individual cases will vary. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making any investment decision, you should consult with your financial advisor about your individual situation.

The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Any opinions are those of author and not necessarily those of Raymond James.

Not all strategies mentioned are suitable for all investors. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

Matching contributions from your employer may be subject to a vesting schedule. Please consult with your financial advisor for more information.

401(k) plans are long-term retirement savings vehicles. Withdrawal of pre-tax contributions and/or earnings will be subject to ordinary income tax and, if taken prior to age 59 1/2, may be subject to a 10% federal tax penalty.

Unless certain criteria are met, Roth IRA owners must be 59½ or older and have held the IRA for five years before tax-free withdrawals are permitted. Additionally, each converted amount may be subject to its own five-year holding period. Converting a traditional IRA into a Roth IRA has tax implications. Investors should consult a tax advisor before deciding to do a conversion.

Please note, changes in tax laws may occur at any time and could have a substantial impact upon each person’s situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.